Financial stress is the psychological strain that results from concerns about one’s financial situation. For farm households, this strain is not incidental; it is a measurable and prominent feature of agricultural life. Most agricultural economists use financial ratios and/or profitability to measure farm financial stress. The financial stress measure used for this article, the APR Financial Stress Scale, was developed and validated by Heo, Cho, and Lee (2020). It captures three dimensions of financial stress, Affective (worry, anxiety), Physiological (sleep disruption, physical tension), and Relational (strain on family and social relationships), offering a more complete picture than measures focused on income or debt alone.

For farmers, this matters because financial stress is rarely “just” a numbers problem. It can show up as difficulty sleeping during planting or harvest season, tension in family decision-making about the operation, or a persistent sense of worry that does not lift even when the books technically balance.

The Data

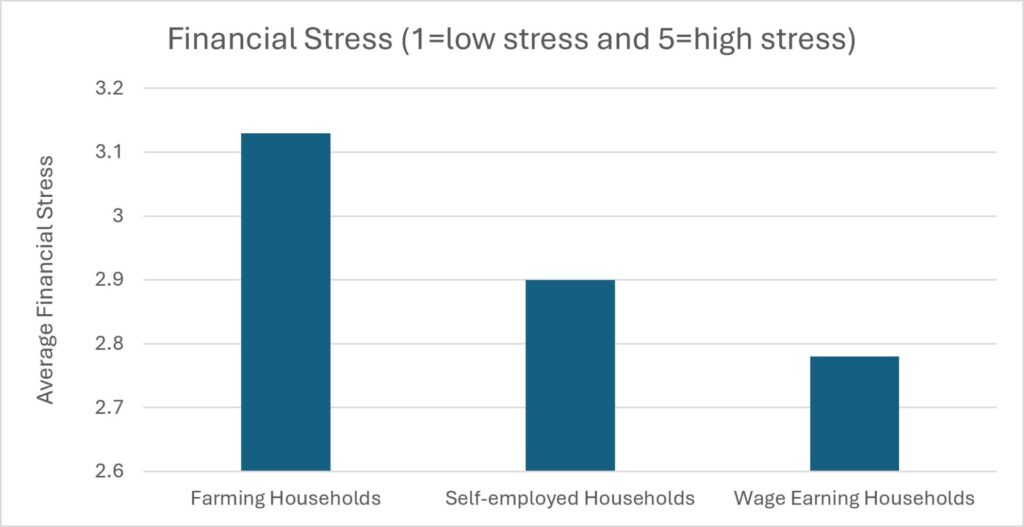

Using the NCR-Stat: Baseline 2024 data from households in the Midwest, South, and Northeast regions of the U.S. (N = 14,039), I compared financial stress scores between farming and non-farming households. Farmers reported a mean financial stress score of 3.13 (SD = 1.14), compared to 2.79 (SD = 1.12) among non-farmers. This difference of 0.34 points was statistically significant, indicating that farmers experience meaningfully higher levels of financial stress than the general population.

I also compared farming households to other self-employed households, who had a mean stress score of 2.90 (SD = 1.07). Farmers still had statistically significantly higher levels of financial stress. The chart below demonstrates the different levels of financial stress for farmers, non-farm self-employed, and wage-earning households.

Source: NCRCRD NCR-Stat Database

This pattern is consistent with what farm families already know from lived experience: input costs, commodity price volatility, weather risk, and the seasonal, often unpredictable nature of farm income create a distinct financial burden that does not map neatly onto the steady-paycheck assumptions built into most financial guidance.

What This Means for Farm Families

The first step is recognizing that financial stress is a legitimate and measurable health concern, rather than a personal failing. Some of the most common symptoms of financial stress can include missing critical operational windows, withdrawal, increased forgetfulness, unusual outbursts of anger, sleep disruption, weight changes, or excessive drinking. The elevated rates of financial stress documented in this article demonstrate that, if you are experiencing these symptoms, you are not alone. High financial stress reflects the structural features of agriculture rather than individual shortcomings. If you notice persistent financial worry, sleep problems tied to financial concerns, or growing tension at home around money, you are encouraged to reach out to local resources such as Extension offices, the Purdue Extension Farm Stress Team, the North Central Farm and Ranch Stress Assistance Center, or other local behavioral health resources. Many states offer confidential farm crisis hotlines and financial counseling at no cost.

References

Bednarik, Z.; Green, J. J.; Marshall, M. I.; Russell, K. J.; Wiatt, R. D.; Wilcox Jr, M. D. (2026). North Central Region Household Data. NCR-Stat: Baseline Survey 2024. Purdue University Research Repository. doi:10.4231/NQG5-5V79

Heo, W., Cho, S. H., & Lee, P. (2020). APR Financial Stress Scale: Development and validation of a multidimensional measurement. Journal of Financial Therapy, 11(1). https://doi.org/10.4148/1944-9771.1216